Airlines Are Charting Different Courses. Cash Could Decide the Winner.

There is no single operating manual that airlines are using to fly through the pandemic. Where foresight fails to yield results, though, cash could lend a hand.

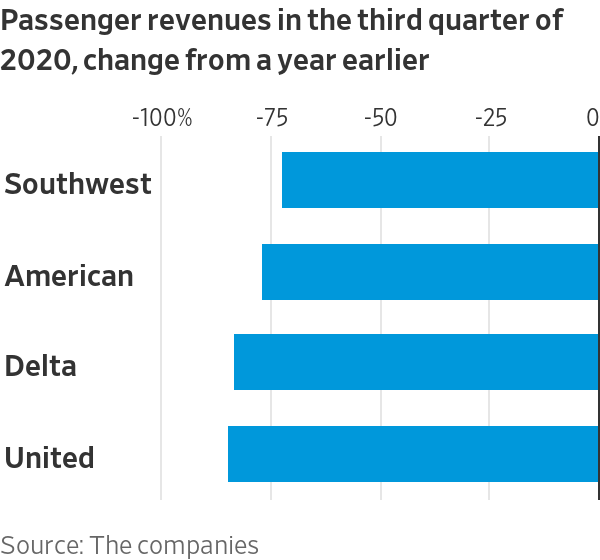

The big four U.S. carriers together lost about $11 billion in the third quarter, as a resurgence of coronavirus cases delayed the recovery in air travel. They have been forced to cut more flights from their schedules and push back the date at which they expect to stop burning cash.

Markets have so far chosen to be optimistic, whether due to top-down investment trends, hopes of further government aid or signs that willingness to travel may be improving ahead of Thanksgiving and Christmas. The Dow Jones U.S. Airlines Index is up 6% since

Delta Air Lines

kicked off the earnings season on Oct. 13.

Capitalizing on scarce domestic demand, however, can be approached very differently. The latest results confirm just how divergent airline strategies have become.

American stands out as the nimblest of the three legacy carriers. Like low-cost operators, it has sought to revive sales by chasing short-term demand trends, such as point-to-point routes to sunny spots like Florida and Mexico. While third-quarter passenger revenues at Delta and

United Airlines

fell 83% and 84% from a year earlier, respectively,

American Airlines

’ dropped 77%. Budget leader Southwest reported a similar figure. American’s planes were almost 60% full, far more than other major airlines.

Competing with low-cost operators, though, is a double-edged sword, especially during a pandemic. Most of the third-quarter sales were to last-minute bookers at big discounts. To fill seats, American had to lower its average fare per passenger per mile by more than 25%, twice the drop reported by Delta and United. Even

Southwest Airlines

discounted less. Yet American’s operating costs are much higher, so it is losing more money relative to sales.

There are also points of strategic divergence between the two more conservative full-service players. United has included point-to-point routes in its winter schedule, and confirmed last week that it won’t permanently retire aircraft to remain flexible. This will make it easier to gain market share quickly as soon as a Covid-19 vaccine is found, but could lead to steeper costs in the meantime. By contrast, Delta has focused on reinforcing its hubs and recently emphasized efforts to reduce its fleet.

Meanwhile, Southwest is attacking airports traditionally dominated by legacy carriers, such as United’s hubs in Chicago and Houston and American’s in Miami. It intends to emerge from the pandemic with a bigger share of business travel, even though this source of revenues remains very limited for the foreseeable future.

Such network strategies are key to identifying which airlines will ultimately wrest profits from others. But investors shouldn’t forget that making the right decisions now could end up being less important than preserving the ability to make them later, when the crisis finally ends. To achieve that, the only real flexibility involves having the money to course-correct. In this department, Southwest and Delta still tower above the rest.

Cash was king during the depths of the crisis this spring. When demand eventually recovers for airlines, it could be an even bigger game-changer.

Third-quarter passenger revenue at Delta fell 83% from a year earlier.

Photo: michael reynolds/Shutterstock

Write to Jon Sindreu at jon.sindreu@wsj.com